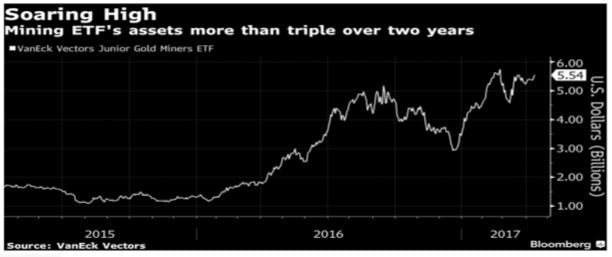

The junior gold miner ETF has gotten too big for its own good; The inflow of money has created a serious problem for GDXJ; It simply has too much capital in proportion to its limited market space (Exhibit 1) The ETF's index is making changes that will cause performance to drag, and its mission to creep. GDXJ: Too big for its own goodGDXJ is in an unsustainable position. With $5.5B in assets, the ETF has to buy a whopping 20% of the junior miners sector. Thus, it can’t trade in and out of positions without sending prices to the moon/floor when the index changes and forces it to add or drop a position. Its largest holding Alamos Gold (AGI) is just a 5% portfolio position within GDXJ, however this same stake amounts to 13% of Alamos’s total outstanding shares. Combining GDXJ’s holdings in GDX, the junior miner index owns more than 20% of Alamos, getting near the threshold that might trigger a mandatory share tender under Canadian law. To combat oversized positions in individual stocks, GDXJ has deviated from its index. This is problematic in itself as an index investor; you expect to get the returns of the index minus the management fee. With GDXJ, you’re potentially getting major slippage since they haven’t followed the index. GDXJ’s third largest holding is GDX. This is deeply problematic, as you get exposure to the big boys, and sets the stage for multiplication of fees. Broader problems lie ahead for indexing. Indexing spreads money around without due diligence. Anything that meets the mechanical criteria for index inclusions gets a flood of passive money. GDXJ itself ran into problems in 2013 when a 5% holding (LionGold) was in fact a sham, and the share price collapsed overnight. Due to index funds putting bigger positions on stocks as market caps rise structurally, there’s reason for ETFs to throw lots of money at hot momentum stocks such as LionGold that later collapse. An imperfect solution With no sign that the flood of money into junior miners will end, the ETF will now be expanding its current addressable market of stocks from $30B to $70B. This should avoid concentration risk at least for the time being. This solution is far from perfect. For one it distorts the ETF’s reason for being. Investors want exposure to juniors, yet have to accept a larger weighting in big caps. More alarmingly, GDXJ will be making a massive and messy portfolio reallocation in June. According to BMO Capital Market’s research, GDXJ will add roughly 18 new component names, and BMO has suggested that GDXJ sell more than half of its current holdings (roughly $3B), in order to fund the new positions. This is a tragedy for ETF holdings. For one, they would be hit with significant tax consequences of an ETF engaging in such a high rate of portfolio turnover. Additionally, arbitrage traders are able to take advantage of forced shifts in ETF positioning by buying the new additions and shorting the deletions. ConclusionAs a result of these risks, it is likely a better idea to buy a basket of good junior miners within the industry, rather than buying the increasingly defective ETF. Forgoing the 0.52% expense ratio should more than cover additional trading costs. Note: GDX is not in this situation. The biggest miners like ABX are twice the size of GDX itself, thus GDX can have a 5% stake in ABX and only own 2.5% of Barrick- the company. GDXJ by contrast was more than 2x as big as its largest investment- thus 5% of portfolio stake in Alamos turned into owning 13% of the company. That is not sustainable. Exhibit 1  Comments are closed.

|

About the O&G Research TeamThe O&G Research Team publishes insights on the global markets. Our research scope ranges from the US to China. Categories

All

Follow us on WeChat:

Read new articles and updates everyday on your phone!

DisclosuresWe may invest in some of the companies mentioned on this website. We are not responsible for the content on any external links on this website. The opinions expressed in this report do not constitute a buy or sell recommendation.

|

RSS Feed

RSS Feed